Workers Compensation Insurance | Buy Workers Compensation Insurance. Get Fast, Free Work Comp Quotes!

Workers Compensation Insurance

Protect your business and team with workers’ comp. Get a workers compensation policy… fast!

Learning Center

View All

This website is powered by Work Comp Brokers, Inc., a leading independent work comp insurance brokerage since 2004. ...

Workers’ compensation, also known as workmans’ comp, is a state-mandated insurance program that provides benefits to employees who ...

Workers’ Compensation insurance is one of the most significant expenses for businesses, particularly for high risk industries with ...

Workers’ Comp Insurance is a common thread for businesses with employees, it also means the cost of this ...

Pay As You Go billing integrates your Workers’ Compensation premium directly to your payroll software and automatically submits small payments to ...

A workers compensation class code is a four digit numerical code assigned by NCCI or a State Rating ...

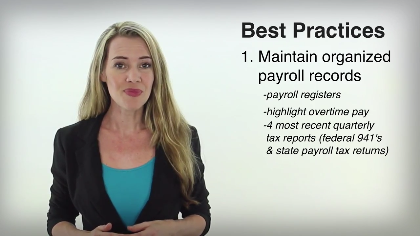

Everyone hates the word, “AUDIT!” Unfortunately, it’s a requirement of the workers compensation policy process. The audit is ...

Jail? Fines? Your penalty will depend on three things….

An experience rating modification, commonly called “MOD”, is an important factor used to adjust your workers’ compensation premium. ...